- BLOG

- BLOCKCHAINS

- Miners Income and Future of Bitcoin

Miners Income and Future of Bitcoin

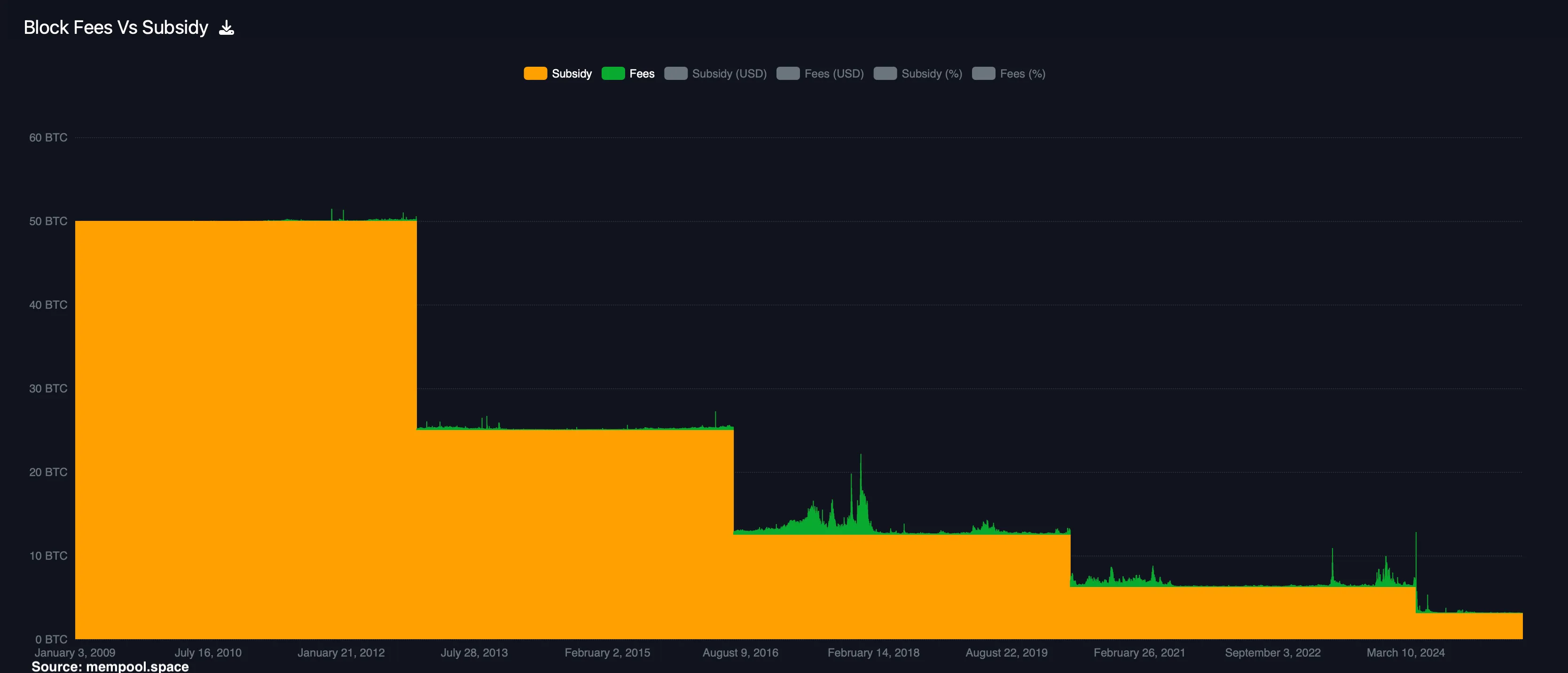

What can we see on this chart? In essence, it represents the revenue breakdown of the whole Bitcoin mining industry. And it provides a glimpse into possible future of Bitcoin. Which, contrary to the public hype, may not be as bright as many believe.

What can we see on this chart? In essence, it represents the revenue breakdown of the whole Bitcoin mining industry. And it provides a glimpse into possible future of Bitcoin. Which, contrary to the public hype, may not be as bright as many believe.

Two sources of Bitcoin-miner revenue

Bitcoin miners live on two pay checks: block subsidies - which are newly minted BTC that halve roughly every four years (the yellow areas on the chart), and transaction fees paid by users who want their transfers confirmed (green spiky areas). Each Halving (a visible steps on the yellow ladder) cuts the subsidy in half and leaves miners hoping that either price jumps or fees rise to fill the gap. Fees do spike during traffic jams and occasional events like Ordinals launch, but the average remains insignificant, so the long-term trend is clear: subsidies shrink while fee growth is lumpy.

Digital Gold vs. Digital Cash and the Block-Size Wars

Satoshi’s dream vision for Bitcoin was uncensored “digital cash.” A decade later, most of the community re-cast Bitcoin as “digital gold,” a hedge against fiat debasement. The 2015-17 Block-Size Wars settled the debate: big-block advocates lost, the 1 MB cap stayed, and high-frequency retail payments migrated to Layer-2 experiments like Lightning or to NFT experiments such as Ordinals and Runes. The chain now processes roughly seven on-chain transactions per second, which is hardly coffee-shop money. Bitcoin is nowhere near to being “digital cash”.

The Future

Now Bitcoin’s “digital gold” narrative is being cemented by Wall Street even further. U.S. spot ETFs from BlackRock, Fidelity, and others already hold well over 500 000 BTC, or about 2.4% of the eventual supply, and inflows regularly pierce $1 billion in a single day. Corporations like Michael Sailor’s Strategy, big funds, and treasuries together control more than 6% of outstanding coins, a share that keeps climbing.

Yet Bitcoin miners face arithmetic they cannot dodge. Subsidies will keep falling toward zero, and fee income is too volatile and genuinely insufficient to guarantee payroll. Hash-rate records above 800 EH/s show that big, efficient farms are outcompeting smaller rivals; five listed miners now capture more than one-fifth of all block rewards. Bankruptcies and fire-sale mergers like Argo Blockchain, Core Scientific, Rhodium signal an industry already in forced consolidation. Fewer pools, more institutional wallets: decentralisation’s iron triangle is tightening.

If block production and token ownership both cluster in a handful of corporations, Bitcoin could drift further from Satoshi’s anti-establishment ethos, and a confidence shake-out could follow. A wave of selling from small holders could depress the market price and slice miner revenues again, accelerate further consolidations, and reinforce the very concerns that sparked the sell-off. A classic reflexive loop.

Conclusion

Is this bleak scenario inevitable? No. Is it plausible? Absolutely. Keep an eye on Bitcoin transaction fees, miners diversity, and corporate treasuries hunger; the health of those three metrics will sketch the real path ahead for Bitcoin.

How to Use Hyperliquid: Complete Guide to Trading, Vaults, and Staking (2025)

Prediction Markets Explained: History, Polymarket, Futarchy, and Tax Implications (2025 Guide)